Practical Finance and Data Analysis Lab Summary

Here is the lab manual page.

Here are my lab notes.

Partner: Justin Muehlmeyer

Introduction

This lab was basically undefined to start with, with simple goals of gathering knowledge on finance in general, learning where to find data, and using data analysis methods to glean information from the data. We came up with several grand ideas, but finally condensed our goals- the entire process can be seen in the lab notes.

Approach

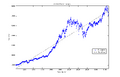

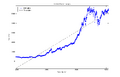

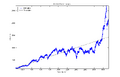

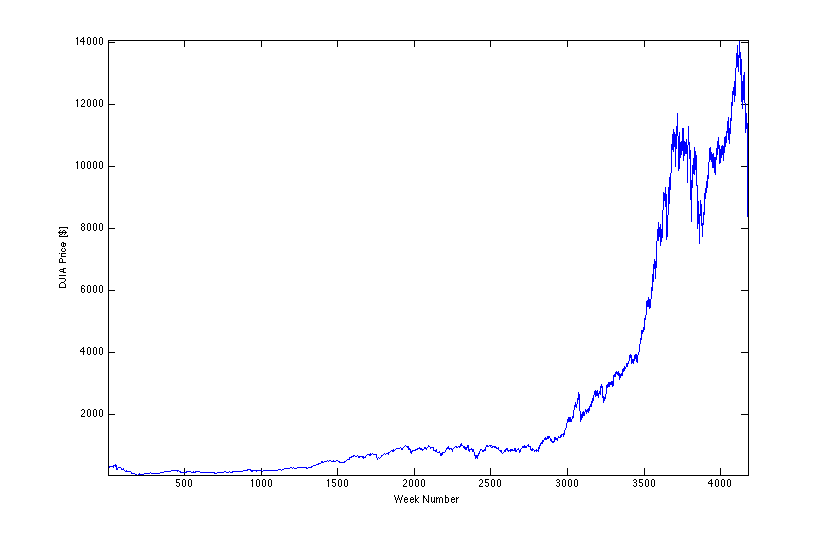

In the end, we generated fixed-length time windows with random start dates over the period of price data acquired for the Dow Jones Industrial Average, then tried to find an average growth rate using both "snapshots" and least-squares linear fits. We defined snapshots as slopes between the start and end points in each time window, reflecting what a person would receive if he actually invested over exactly each window. Least-squares fits take into account fluctuations in the price between the start and end points, so that someone investing on a shorter interval would probably see results more akin to the least-squares fit of his specific time window. We compared the two methods over several different time windows, then analyzed the least-squares data to see if it fit any sort of distribution.

Final Results

Least-squares:

| Least-squares Slope Data [$/week] ± σravg

|

Sample Window

|

| 10 Year Window

|

| 1) 2.4689 ± 0.0007

|

11) 2.6043 ± 0.0007

|

| 2) 3.1063 ± 0.0011

|

12) 3.2287 ± 0.0011

|

| 3) 2.5977 ± 0.0008

|

13) 2.1363 ± 0.0009

|

| 4) 2.4893 ± 0.0007

|

14) 2.8116 ± 0.0008

|

| 5) 2.8451 ± 0.0007

|

15) 2.3922 ± 0.0005

|

| 6) 2.1571 ± 0.0007

|

16) 2.7420 ± 0.0009

|

| 7) 3.0676 ± 0.0009

|

17) 3.1118 ± 0.0008

|

| 8) 3.4700 ± 0.0009

|

18) 2.4796 ± 0.0009

|

| 9) 2.1050 ± 0.0006

|

19) 2.3554 ± 0.0009

|

| 10) 2.2250 ± 0.0008

|

20) 2.0223 ± 0.0009

|

|

|

| 20 Year Window

|

| 1) 2.9810 ± 0.0003

|

11) 2.5314 ± 0.0003

|

| 2) 2.8751 ± 0.0004

|

12) 2.5233 ± 0.0003

|

| 3) 2.1529 ± 0.0003

|

13) 2.0260 ± 0.0003

|

| 4) 2.5026 ± 0.0002

|

14) 2.8666 ± 0.0003

|

| 5) 2.3646± 0.0002

|

15) 2.8161 ± 0.0003

|

| 6) 3.5018 ± 0.0004

|

16) 2.0481 ± 0.0003

|

| 7) 2.3696 ± 0.0002

|

17) 2.8723 ± 0.0003

|

| 8) 2.7557 ± 0.0003

|

18) 2.6072 ± 0.0003

|

| 9) 2.0702 ± 0.0003

|

19) 3.0362 ± 0.0004

|

| 10) 2.6607 ± 0.0003

|

20) 1.8809 ± 0.0003

|

|

|

| 30 Year Window

|

| 1) 1.6386 ± 0.0002

|

11) 1.7714 ± 0.0002

|

| 2) 1.6168 ± 0.0002

|

12) 1.9832 ± 0.0002

|

| 3) 1.9087 ± 0.0002

|

13) 1.7668 ± 0.0002

|

| 4) 1.4801 ± 0.0002

|

14) 1.2027 ± 0.0002

|

| 5) 1.8070 ± 0.0002

|

15) 2.0399± 0.0002

|

| 6) 2.3613 ± 0.0002

|

16) 1.9900 ± 0.0002

|

| 7) 1.9316 ± 0.0002

|

17) 2.1310 ± 0.0002

|

| 8) 2.3433 ± 0.0002

|

18) 2.3271 ± 0.0002

|

| 9) 2.1834 ± 0.0002

|

19) 2.1681 ± 0.0002

|

| 10) 1.6845 ± 0.0002

|

20) 1.9814 ± 0.0002

|

|

|

| 40 Year Window

|

| 1) 1.2491 ± 0.0002

|

11) 1.5066 ± 0.0002

|

| 2) 1.6391 ± 0.0002

|

12) 1.6332 ± 0.0002

|

| 3) 1.4006 ± 0.0002

|

13) 1.7675 ± 0.0002

|

| 4) 1.6526 ± 0.0001

|

14) 1.7078 ± 0.0002

|

| 5) 1.8456 ± 0.0002

|

15) 1.4713 ± 0.0002

|

| 6) 1.4773 ± 0.0002

|

16) 1.6195 ± 0.0002

|

| 7) 1.5594 ± 0.0001

|

17) 1.6892 ± 0.0002

|

| 8) 1.5667 ± 0.0002

|

18) 1.5924 ± 0.0002

|

| 9) 1.6973 ± 0.0001

|

19) 1.7595 ± 0.0002

|

| 10) 1.3066 ± 0.0002

|

20) 1.3776 ± 0.0002

|

|

|

| 50 Year Window

|

| 1) 1.5937 ± 0.0001

|

11) 1.4359 ± 0.0002

|

| 2) 1.3238 ± 0.0002

|

12) 1.4196 ± 0.0002

|

| 3) 1.5460 ± 0.0001

|

13) 1.5010 ± 0.0001

|

| 4) 1.4301 ± 0.0002

|

14) 1.6835 ± 0.0002

|

| 5) 1.4891 ± 0.0002

|

15) 1.4429 ± 0.0001

|

| 6) 1.3474 ± 0.0001

|

16) 1.4743 ± 0.0001

|

| 7) 1.6312 ± 0.0002

|

17) 1.4178 ± 0.0001

|

| 8) 1.4696 ± 0.0002

|

18) 1.5034 ± 0.0002

|

| 9) 1.5794 ± 0.0001

|

19) 1.4420 ± 0.0001

|

| 10) 1.3559 ± 0.0001

|

20) 1.3633 ± 0.0001

|

|

|

| Window

|

Average Least-squares Slope after 100 iterations and 20 Trials ($/week)

|

| 10 Year

|

2.782 ± .0002

|

| 20 Year

|

2.442 ± .0001

|

| 30 Year

|

1.916, error < .0001

|

| 40 Year

|

1.576, error < .0001

|

| 50 year

|

1.472, error < .0001

|

Snapshot:

| Snap Shot Window

|

Average Slope after 100 iterations and 20 Trials ($/week)

|

| 10 Year

|

2.997

|

| 20 Year

|

2.287

|

| 30 Year

|

2.002

|

| 40 Year

|

1.892

|

| 50 year

|

1.999

|

The snapshot and least-squares methods are roughly comparable, although not within error bars generated with least-squares fitting. I believe more iterations of the snapshot method would be necessary to make up for its lack of sensitivity of trends. This would in a sense be a "least-squares" analysis taking a much longer route.

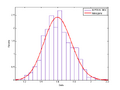

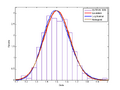

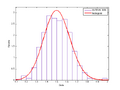

Distribution

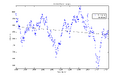

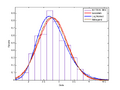

The least-squares data returned histograms with leftward-leaning "shoulders," which make sense given the preponderance of smaller slope in the total time period of the DJIA price:

With this in mind, fitting with known distributions seemed frivolous, but did provide elementary insight into the distribution fitting process in general. The log-likelihood rating given fits intrigues me in particular, but online resources are cryptic at best. Open science has not conquered this one just yet!

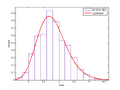

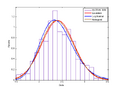

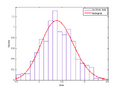

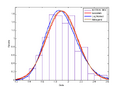

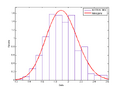

Examples of fits I tried on 500 iterations of average rates:

| 500 Iteration Probability Distribution

|

Fit Parameters

|

|

|

10 year:

Distribution: Normal

Log likelihood: -336.618

Domain: -Inf < y < Inf

Mean: 2.79947

Variance: 0.225507

Parameter Estimate Std. Err.

mu 2.79947 0.0212371

sigma 0.474876 0.0150395

Estimated covariance of parameter estimates:

mu sigma

mu 0.000451013 -1.07538e-18

sigma -1.07538e-18 0.000226185

Distribution: Lognormal

Log likelihood: -332.103

Domain: 0 < y < Inf

Mean: 2.79986

Variance: 0.231355

Parameter Estimate Std. Err.

mu 1.01503 0.00762697

sigma 0.170544 0.00540119

Estimated covariance of parameter estimates:

mu sigma

mu 5.81707e-05 -3.97263e-19

sigma -3.97263e-19 2.91729e-05

Distribution: Nakagami

Log likelihood: -332.751

Domain: 0 < y < Inf

Mean: 2.79988

Variance: 0.222772

Parameter Estimate Std. Err.

mu 8.91723 0.553746

omega 8.0621 0.120739

Estimated covariance of parameter estimates:

mu omega

mu 0.306634 1.83823e-09

omega 1.83823e-09 0.014578

|

|

|

20 year:

Distribution: Normal

Log likelihood: -189.022

Domain: -Inf < y < Inf

Mean: 2.41135

Variance: 0.124957

Parameter Estimate Std. Err.

mu 2.41135 0.0158086

sigma 0.353492 0.0111952

Estimated covariance of parameter estimates:

mu sigma

mu 0.000249913 2.0193e-19

sigma 2.0193e-19 0.000125333

Distribution: Lognormal

Log likelihood: -190.842

Domain: 0 < y < Inf

Mean: 2.41174

Variance: 0.13012

Parameter Estimate Std. Err.

mu 0.869288 0.00665194

sigma 0.148742 0.0047107

Estimated covariance of parameter estimates:

mu sigma

mu 4.42483e-05 2.60163e-21

sigma 2.60163e-21 2.21907e-05

Distribution: Nakagami

Log likelihood: -187.868

Domain: 0 < y < Inf

Mean: 2.41137

Variance: 0.124614

Parameter Estimate Std. Err.

mu 11.7865 0.735135

omega 5.93933 0.0773678

Estimated covariance of parameter estimates:

mu omega

mu 0.540424 2.95263e-09

omega 2.95263e-09 0.00598578

|

|

|

30 year:

Distribution: Normal

Log likelihood: 6.36398

Domain: -Inf < y < Inf

Mean: 1.90213

Variance: 0.0571925

Parameter Estimate Std. Err.

mu 1.90213 0.0106951

sigma 0.239149 0.00757394

Estimated covariance of parameter estimates:

mu sigma

mu 0.000114385 1.29821e-18

sigma 1.29821e-18 5.73646e-05

Distribution: Lognormal

Log likelihood: 7.37713

Domain: 0 < y < Inf

Mean: 1.90226

Variance: 0.058345

Parameter Estimate Std. Err.

mu 0.635044 0.00565599

sigma 0.126472 0.0040054

Estimated covariance of parameter estimates:

mu sigma

mu 3.19902e-05 -1.3048e-19

sigma -1.3048e-19 1.60432e-05

Distribution: Nakagami

Log likelihood: 7.99048

Domain: 0 < y < Inf

Mean: 1.90219

Variance: 0.0568658

Parameter Estimate Std. Err.

mu 16.0294 1.00341

omega 3.67519 0.0410522

Estimated covariance of parameter estimates:

mu omega

mu 1.00684 2.23054e-09

omega 2.23054e-09 0.00168528

|

|

|

40 year:

Distribution: Normal

Log likelihood: 191.058

Domain: -Inf < y < Inf

Mean: 1.60399

Variance: 0.0273207

Parameter Estimate Std. Err.

mu 1.60399 0.00739199

sigma 0.16529 0.00523478

Estimated covariance of parameter estimates:

mu sigma

mu 5.46414e-05 -3.82513e-19

sigma -3.82513e-19 2.74029e-05

Distribution: Lognormal

Log likelihood: 191.951

Domain: 0 < y < Inf

Mean: 1.60404

Variance: 0.0276637

Parameter Estimate Std. Err.

mu 0.46718 0.00462479

sigma 0.103413 0.00327514

Estimated covariance of parameter estimates:

mu sigma

mu 2.13887e-05 -1.04169e-19

sigma -1.04169e-19 1.07265e-05

Distribution: Nakagami

Log likelihood: 192.237

Domain: 0 < y < Inf

Mean: 1.60402

Variance: 0.0271876

Parameter Estimate Std. Err.

mu 23.7815 1.49365

omega 2.60005 0.0238439

Estimated covariance of parameter estimates:

mu omega

mu 2.23098 2.58228e-09

omega 2.58228e-09 0.000568533

|

|

|

50 year:

Distribution: Normal

Log likelihood: 316.326

Domain: -Inf < y < Inf

Mean: 1.50232

Variance: 0.0165531

Parameter Estimate Std. Err.

mu 1.50232 0.0057538

sigma 0.128659 0.00407467

Estimated covariance of parameter estimates:

mu sigma

mu 3.31062e-05 -1.89468e-19

sigma -1.89468e-19 1.66029e-05

Distribution: Lognormal

Log likelihood: 317.216

Domain: 0 < y < Inf

Mean: 1.50234

Variance: 0.0166775

Parameter Estimate Std. Err.

mu 0.403344 0.00383718

sigma 0.0858019 0.00271737

Estimated covariance of parameter estimates:

mu sigma

mu 1.47239e-05 -4.44414e-20

sigma -4.44414e-20 7.38411e-06

Distribution: Nakagami

Log likelihood: 317.246

Domain: 0 < y < Inf

Mean: 1.50233

Variance: 0.0164799

Parameter Estimate Std. Err.

mu 34.3622 2.1628

omega 2.27348 0.0173446

Estimated covariance of parameter estimates:

mu omega

mu 4.67769 3.29831e-09

omega 3.29831e-09 0.000300836

|

Thoughts

This lab basically turned into a large exercise on data manipulation and information-hunting. I also was able to combine concepts from lecture on linear least-squares fitting with more general error propagation.

The distribution analysis is gratifying in that I see a reflection in the processed data corresponding to trends in the raw data. Something to try regarding the distribution fit would be to generate a fake DJIA from the best-fit distribution function and compare with the real data. I imagine this would involve something like executing our lab process in reverse, generating huge numbers of linear windows with random start dates and distribution-derived slopes. One could then "smooth" all these disjointed, overlapping linear sections into a fake DJIA.